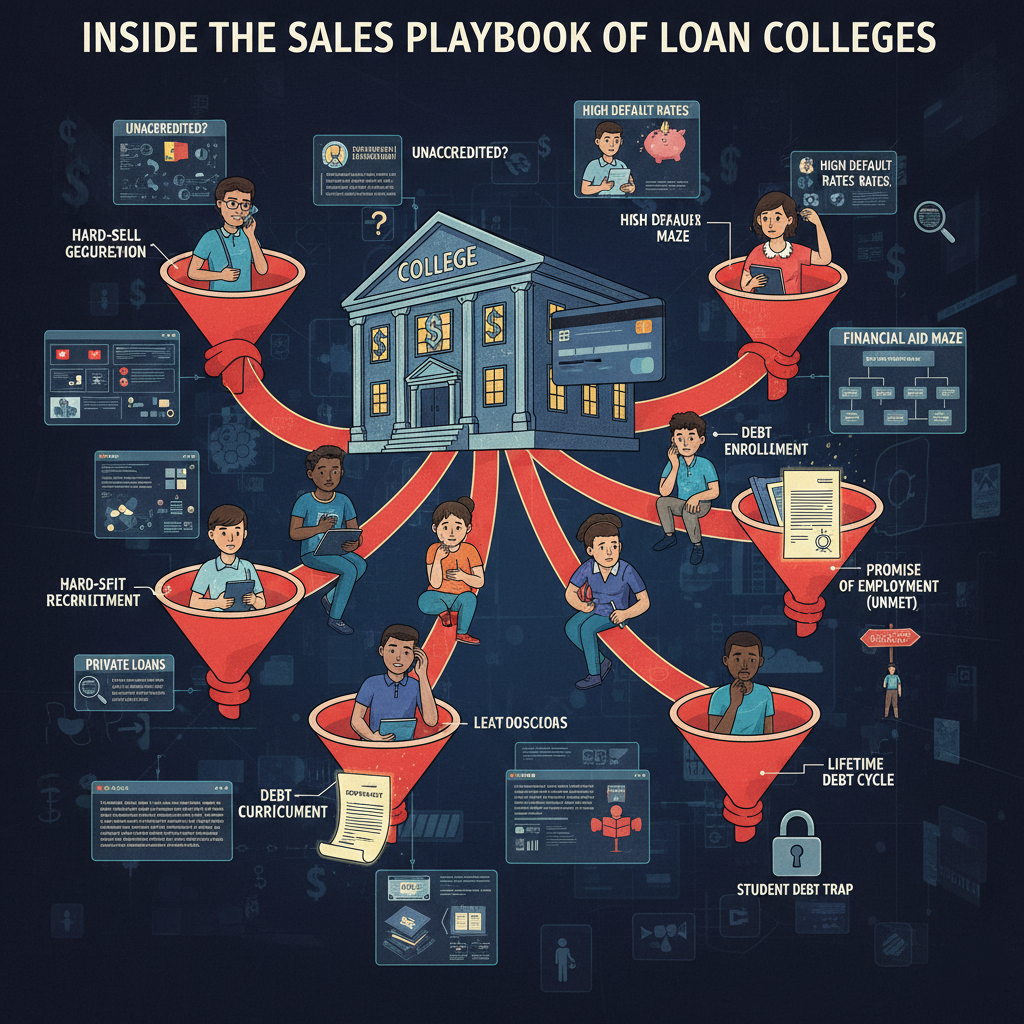

Aggressive Enrollment: Inside the Sales Playbook of Loan Colleges

The call comes at an odd hour.

A cheerful voice, warm and urgent, congratulates you on “taking the first step toward your future.” They already know your name. Your interest. Your hesitation. They speak not like an admissions officer, but like someone trained to close a deal.

This is not an accident.

This is enrollment by design.

When Admissions Became Sales

In many loan-dependent colleges, particularly for-profit and tuition-driven institutions—enrollment is no longer an academic function. It is a revenue engine.

Admissions teams are often trained using the same techniques found in call centers and high-pressure sales floors. Scripts are tested. Conversion rates are tracked. Prospective students are “leads.” Hesitation is treated as an objection to overcome.

Education is the product. Urgency is the tactic.

The Promise That Opens the Door

The pitch is carefully calibrated. It rarely mentions debt upfront. Instead, it centers on transformation.

- “Graduate faster.”

- “Flexible classes for working adults.”

- “Career-ready skills.”

These phrases are not lies—but they are incomplete truths. The emotional appeal comes first, the financial reality later. Sometimes much later.

For students navigating unemployment, family pressure, or economic insecurity, the message lands hard: This is your way out.

Manufacturing Urgency

One of the most powerful tools in the enrollment playbook is time pressure.

Seats are “limited.” Deadlines are “approaching.” Financial aid is framed as something that could disappear if action isn’t taken immediately. The goal is not reflection—it is momentum.

Prospective students are nudged to commit before they fully understand:

- total program cost

- loan terms

- graduation rates

- employment outcomes

Pausing to think becomes framed as self-sabotage.

Personalization as Persuasion

Enrollment counselors are trained to listen closely. Not out of empathy alone, but strategy.

A student mentions wanting to help their parents? The pitch shifts to stability.

A single parent worries about time? Flexibility becomes the headline.

A first-generation student expresses fear? Reassurance fills the gap.

The conversation feels supportive. Intimate, even. But beneath it lies a quiet recalibration—matching emotional vulnerability to the most effective selling point.

The Hand-Off to Debt

Once a student says yes, the process accelerates.

Paperwork is streamlined. Financial aid forms are pre-filled. Loans are normalized. The complexity is handled “for you,” reducing friction and, unintentionally or not, reducing informed consent.

By the time doubt surfaces, enrollment is complete. Classes have started. Withdrawal now feels like failure.

And the debt remains.

Who Bears the Risk

In this system, institutions are paid regardless of outcome.

Lenders are protected by policy.

The student carries the risk—academic, financial, emotional.

If the program underdelivers, the burden does not roll upward. It settles squarely on the borrower’s future.

This asymmetry is not accidental. It is structural.

Selling Hope, Collecting Payments

Aggressive enrollment thrives in the space between aspiration and fear. It does not require deception—only selective emphasis and emotional leverage.

The most troubling part is not that colleges want students. It’s that in some cases, they need students more than students need them.

When education depends on constant intake to survive, enrollment stops being about fit, readiness, or long-term success. It becomes about closing the next call.

Asking the Uncomfortable Question

At what point does encouragement become coercion?

Aggressive enrollment forces us to confront an uneasy truth: when higher education is financed by debt, the line between guidance and sales begins to blur.

And in that blur, the cost of getting it wrong is paid not by the institution—but by the student who believed the pitch.